-

Funds released within 1-2 business days

Funds released within 1-2 business days

-

No property security required

-

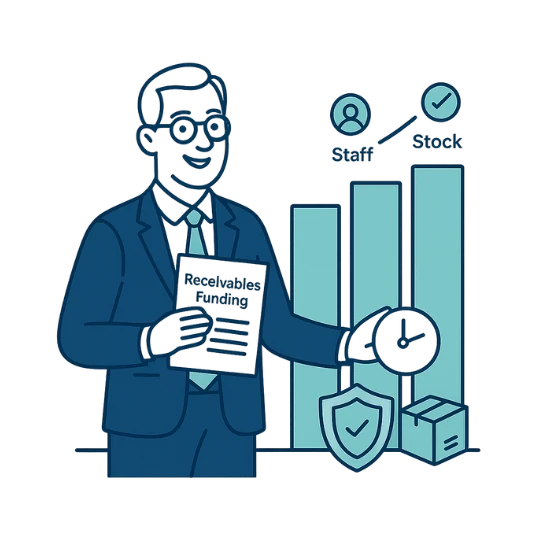

Only pay fees on funds advanced

Leo Navarro

Director, Commercial Painting

Jamie Borg

Owner, Wholesale Supplies

Tahlia Moore

Owner, Supply & Logistics